Housing Market Power Shift Stalls: State-by-State Inventory Divide Widens

Breaking: National Home Inventory Growth Slows, Exposing Regional Gaps

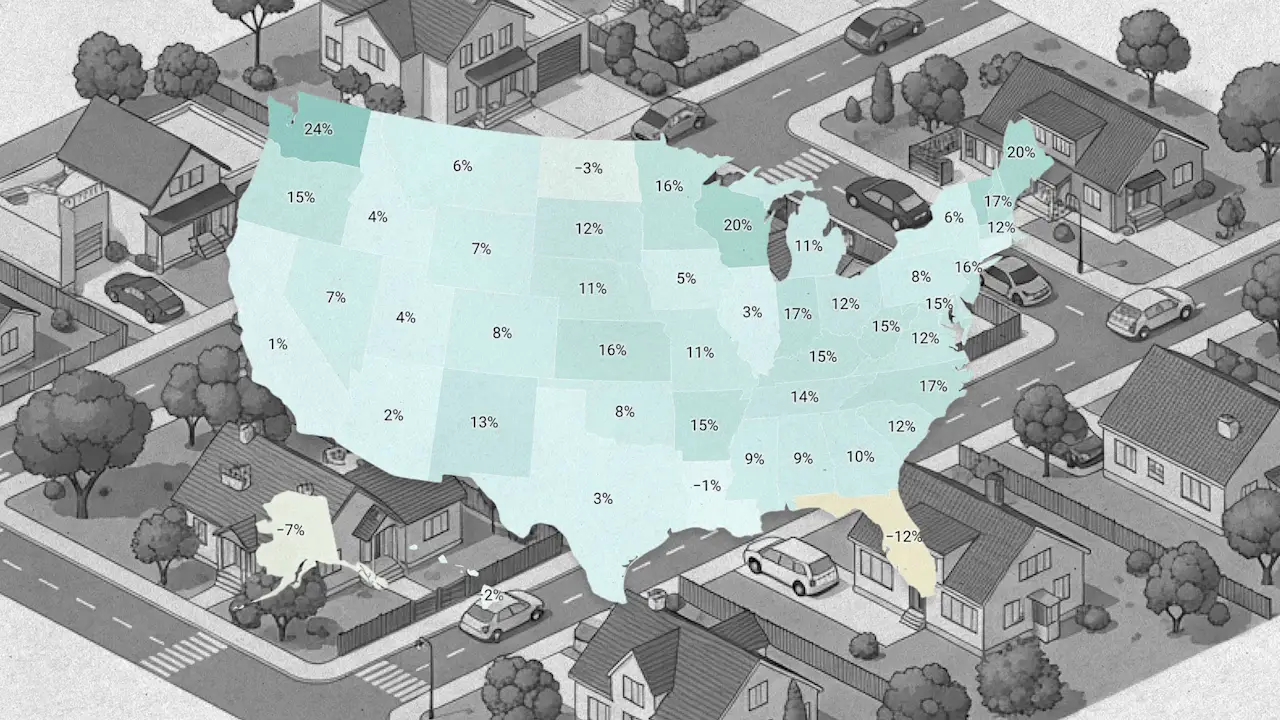

The relentless shift of power from home sellers to buyers across the U.S. housing market has hit a pause. New data from Realtor.com shows that while active listings nationwide rose 4.6% year-over-year as of April 30, 2026, that pace is dramatically slower than the 30.6% surge recorded just 12 months earlier.

This deceleration signals a market in transition. The total inventory of 1,002,935 homes remains 11.8% below pre-pandemic April 2019 levels, according to the report shared exclusively with ResiClub.

Key State-Level Divergence Emerges

Local markets tell a starkly different story. States where active inventory has already climbed above their 2019 benchmarks are seeing softer home prices—or outright declines. In contrast, states where inventory is still far below pre-pandemic levels are experiencing more resilient price growth.

“The national numbers can be misleading,” said Lance Lambert, housing analyst and founder of ResiClub. “In places like Texas or Florida, listings are abundant and giving buyers leverage. But in much of the Northeast and Midwest, inventory remains extremely tight, keeping the upper hand with sellers.”

Background: From Boom to Balance?

The U.S. housing market exploded during the pandemic, with active listings plummeting to just 379,978 in April 2022—a historic low. That frenzy handed sellers almost total control, sparking bidding wars and double-digit price jumps.

Since 2022, that dynamic has slowly reversed. Inventory has climbed back each year, from 562,966 in April 2023 to 734,318 in 2024, and then to 959,251 in 2025. The latest April 2026 figure extends that recovery but at a much slower rate.

The year-over-year growth dropped from +30.6% to just +4.6%. If the current pace of adding roughly 43,684 homes per year continues, inventory would reach 1,046,619 by April 2027—still below 2019 levels.

What This Means for Buyers and Sellers

For homebuyers, the window of improving affordability may be closing in many markets. The slowdown in new listings suggests that sellers in tight-inventory states—particularly across the Midwest and Northeast—are still reluctant to list, keeping competition high and prices elevated.

“Buyers in states like Ohio or New York shouldn’t expect a sudden windfall of choices,” Lambert added. “The inventory deficit is structural there, and it may take years to normalize.”

Sellers in high-inventory states—like Arizona, Florida, and parts of Texas—are already feeling the pressure. Price cuts are becoming more common as homes sit longer on the market. The national months of supply data, while not yet released for April, is expected to show further softening in those regions.

What Experts Are Saying

“This is a market of two halves,” said Zillow senior economist Orphe Divounguy in a separate analysis. “National trends are hiding a much more nuanced picture where local conditions dominate.”

The data underscores that the “power divide” is not just a metaphor—it’s a measurable gap in bargaining leverage, defined by whether a state has recovered its pre-pandemic inventory or remains stuck far below.

ResiClub continues to monitor these trends closely, urging buyers and sellers to ignore national headlines and instead focus on local supply data.